Niger’s Banking Sector Faces Mounting Delinquencies

The January 2026 conjoncture report from the West African Economic and Monetary Union (UEMOA) reveals a stark divide within the regional banking system. While financial institutions grapple with structural weaknesses, Niger stands out as the weakest link, embodying a growing financial rift across the union.

A Disturbing Trend in Asset Degradation

Niger’s banking sector continues to post the most alarming figures in the UEMOA zone. Despite marginal improvements, the country remains the most vulnerable to credit risk, exacerbating regional economic disparities.

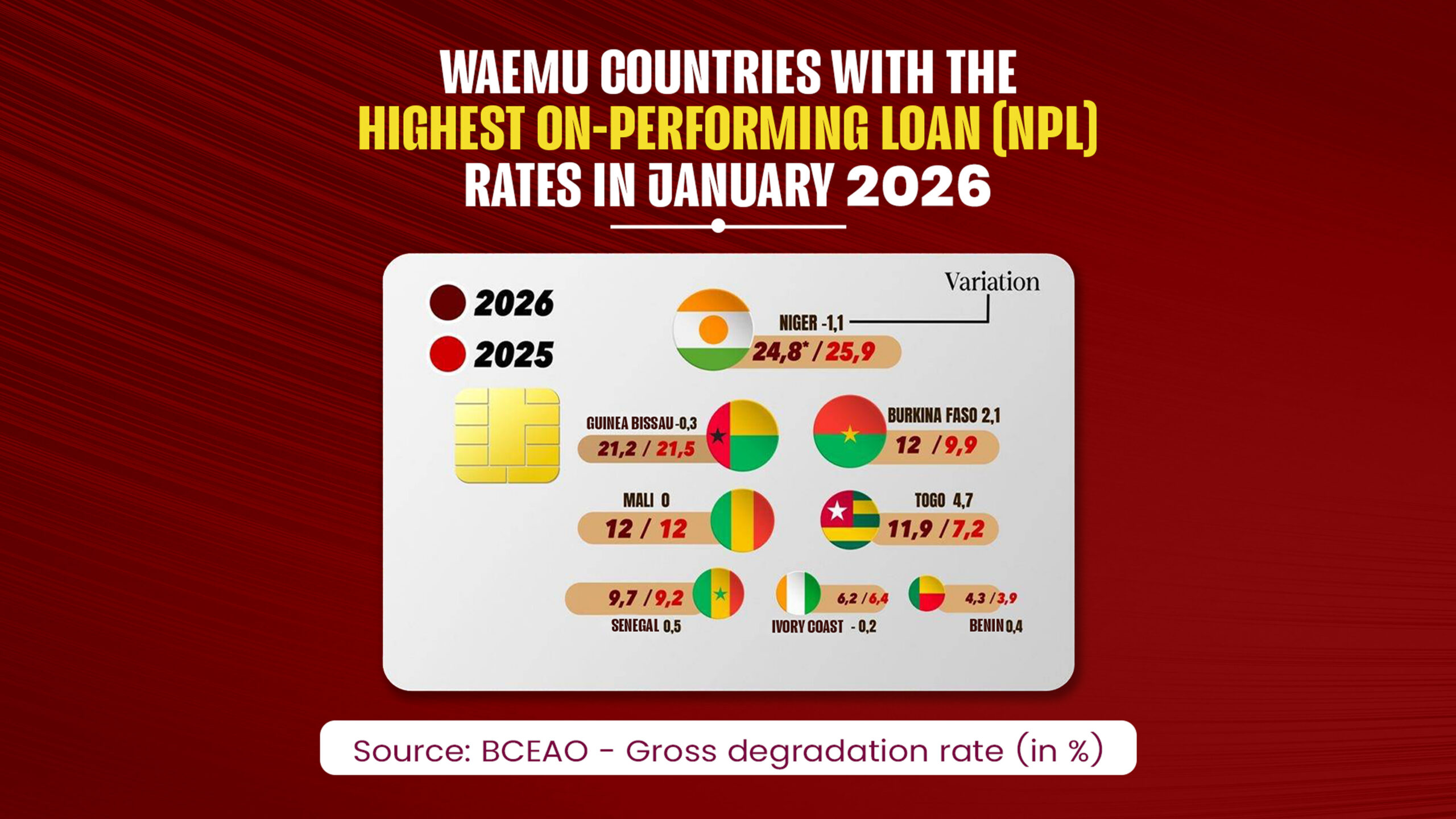

Record-high delinquencies: In January 2026, Niger’s non-performing loan (NPL) ratio reached 24.8%, the highest in the union. Nearly one-quarter of all outstanding loans in the country are now in default, a figure that, while slightly improved from 25.9% in 2025, still vastly exceeds regional averages.

Structural vulnerabilities: The persistently high NPL rate highlights systemic risks, fueled by security challenges and political instability. The gap between Niger’s figures and the regional average underscores an exceptional exposure to financial turmoil.

A Tale of Two Sub-Regions: Coastal vs. Sahelian Economies

The January 2026 data underscores a clear divide between UEMOA’s coastal nations and the Sahelian bloc, with Niger at the epicenter of the crisis.

The Sahelian Bloc Under Strain

Several Sahelian countries are grappling with severe credit deterioration:

- Mali and Burkina Faso: Both report NPL ratios of 12%, with Burkina Faso experiencing a sharp increase of 2.1 percentage points over the past year.

- Guinea-Bissau: The country remains in critical territory with a 21.2% delinquency rate.

Resilience in the Coastal Bloc

In contrast, coastal nations exhibit greater financial stability, though some exceptions persist:

- Benin: Leading the union with the lowest NPL ratio at 4.3%.

- Côte d’Ivoire & Senegal: These economies maintain relative stability, with ratios of 6.2% and 9.7%, respectively.

- Togo’s outlier status: The country defies regional trends with a dramatic surge in delinquencies, rising from 7.2% to 11.9% (+4.7 points).

Regional Credit Growth Clouded by Risk Aversion

The UEMOA’s total outstanding loans crossed a historic threshold of 40.031 trillion FCFA in January 2026, marking a 4.7% annual increase. However, this growth is overshadowed by rising concerns.

Credit risk escalates: Non-performing loans now total 3.631 trillion FCFA, pushing the coverage ratio down to 59%. Banks are struggling to provision for losses at a pace that matches the surge in defaults.

Why the Slowdown?

In response to heightened risks—particularly in Niger—financial institutions have adopted stricter lending policies:

- Tighter eligibility criteria: Banks are demanding higher personal contributions and stricter collateral requirements.

- Selective lending: Institutions are prioritizing balance sheet safety over credit expansion, potentially stifling financing for local SMEs and SMBs.

As of early 2026, the UEMOA banking system stands at a crossroads. While the union’s overall financial stability remains intact, the deteriorating conditions in Niger and the Sahelian bloc demand urgent attention to avert potential liquidity crises.